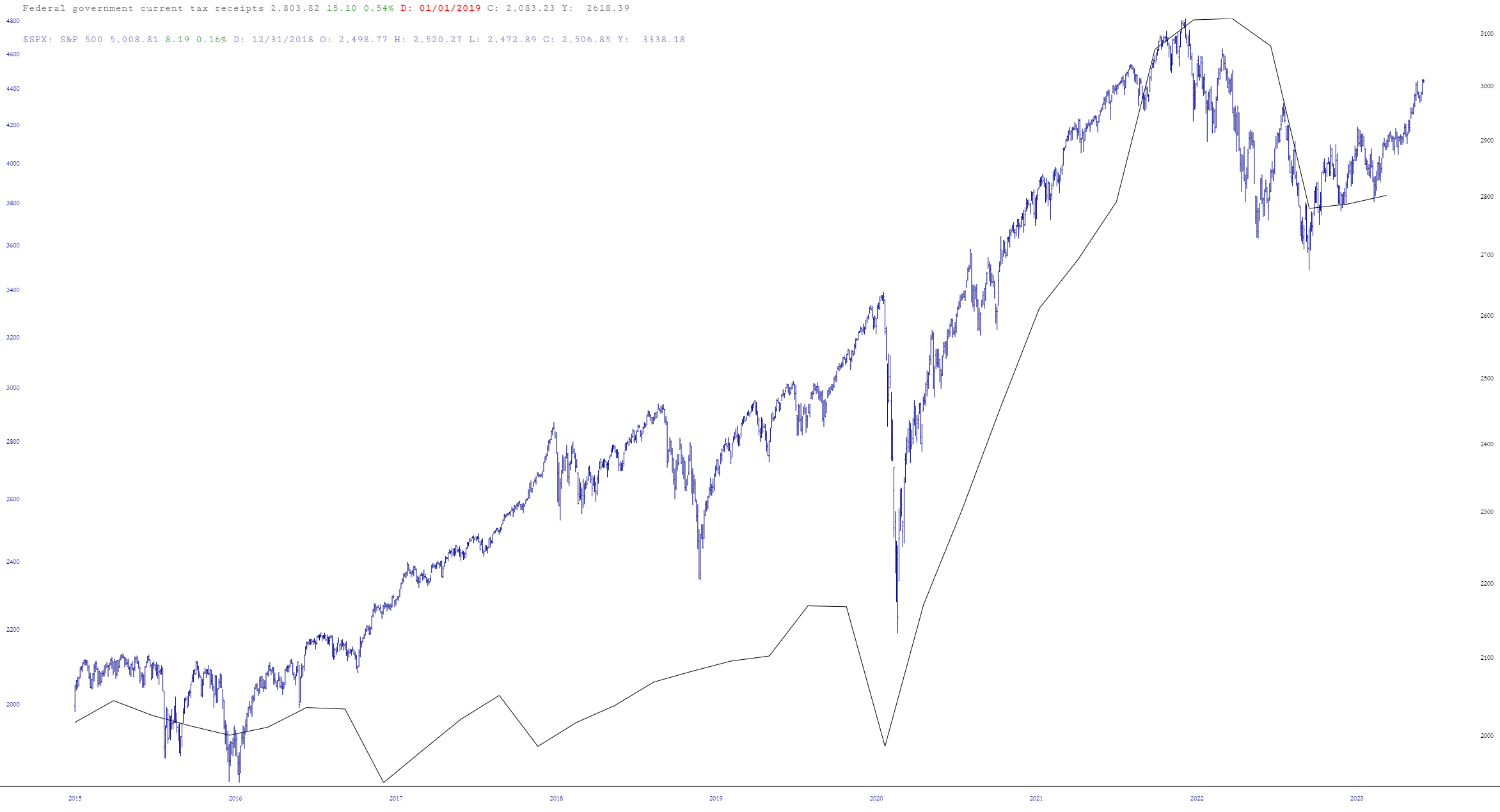

Insufferable data dork and chart nerd that I am, I was curious about the correlation between federal tax receipts and the stock market. Let’s just say they are pretty much joined at the hip:

Here is a closer view. The regrettable thing is that this data is lagging (by definition) and lags quite badly: the latest data point is through Q2 of 2023, so I’m afraid this has zero predictive power. Still, it’s interesting to see that economic health and stocks are still vaguely related, and if you ever hear chatter about tax receipts withering away, you can fully expect equities to do the same.